#In-Depth Guest Blog | The Need to Explore the Finances of Platform Workers

By Rakshith S Ponnathpur

In recent months, there have been several reports on platform workers demanding greater worker rights in India. Platform workers in Chennai, Bengaluru, Hyderabad, and elsewhere, have protested on the streets and on social media to demand better pay, working conditions, and improved social security from platforms.

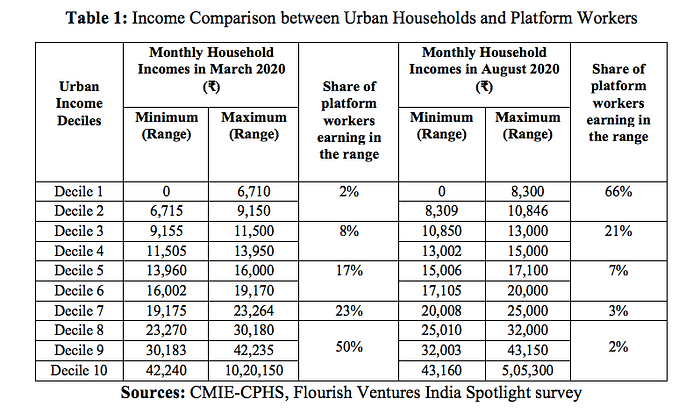

At first sight, surveys carried out before the outbreak of COVID-19 show that more than 75 per cent of the platform workers earned more than ₹20,000 a month, which is substantially higher than what typical, urban, low-income households earned during the same period (less than ₹14,000 a month) (Table 1).[1] However, as I argue in this post, there is a need to understand the financial status-quo of platform workers and their households that go beyond just their absolute earnings. First, I shall outline what is already known about India’s low-income households in general and the urban households in particular, and where the platform workers stand among the larger class of urban, low-income households engaged primarily in informal work. Then, I shall lay out some of the many unanswered questions on platform workers’ finances and discuss why it is crucial to explore them to first get a holistic picture of their financial vulnerabilities and to then deliberate on how to improve their financial well-being.

The Finances of India’s Low-income Households

Indian households, particularly the low-income ones, hold most of their wealth in the form of illiquid, physical assets.[2] They continue to rely on high-interest, informal loans to meet their immediate needs, even though Sharma (2021)’s analysis of the latest All-India Debt and Investment Survey (AIDIS) report points to a considerable shift towards formal loans in recent years. Vishwanath, Dasgupta, and Sharma (2020) have also elucidated other salient characteristics of low-income households that contribute to their overall financial vulnerability.

The Vulnerable yet Under-studied Urban Poor

While a greater focus is paid on rural low-income households both by researchers and policymakers, recent reports have shown that urban low-income households are more vulnerable, with only a few owning any asset of value. In addition, major social protection schemes, such as NREGA, exclusively target the rural poor, leaving the urban poor without an effective safety net. Even other coping mechanisms and financial instruments that exist for the urban poor, like microcredit and Jan Dhan bank accounts, were first designed for the rural poor and later extended as it is to the urban poor. Such replications may not always be suitable remedies for the unique vulnerabilities and constraints faced by the urban poor.

Among the 500 million plus workers in India, only around 20 per cent of them have formal jobs, with the rest dependent on agriculture and other informal sectors in equal measure. While informal workers involved in agriculture mainly reside in rural areas, urban informal workers are mainly involved in trade, hotels, transport, manufacturing and construction sectors, that are characterised by low incomes and lack of job and social security.[3][4] It is this latter segment that mainly comprise the urban low-income households. This means they are frequently exposed to financial shocks. As Dasgupta (2021) has found, these shocks force them to not only exhaust their meager savings but also to constantly seek loans. They are denied opportunities to raise considerable funds to meet their financial goals and find themselves in a perpetual debt trap. This is exacerbated by their reliance on informal finance, both for savings and credit, despite being in closer proximity to a lot more formal financial service providers than their rural counterparts.

Are Platform Workers the same as Urban Poor?

Dvara Research, in partnership with Dvara Money, carried out a literature review on platform workers to get a preliminary understanding of where they stand among the broader category of urban, low-income, informal workers and their households. One of the key takeaways from the exercise was the dearth of exclusive information on the finances of platform workers. Most of the relevant nationally representative datasets like the Periodic Labour Force Survey (PLFS), Consumer Pyramids Household Survey (CPHS), and the All-India Debt and Investment Survey (AIDIS) also do not uniquely identify them. It is only possible to identify low-income households and informal workers, and these generalised findings will have to be applied to platform workers as well.

But existing studies on platform workers, such as this report on platform drivers by Ola Mobility Institute, suggest that close to a half of them usually earn more than ₹1,000 a day, much more than what the urban poor and informal workers typically earn. On the other hand, shocks to the economy also fluctuate their incomes, as do changes in the payment and incentive structures of the platforms themselves. A comparison of the incomes of urban households from the CPHS dataset with those of platform workers from the India Spotlight survey carried out by Flourish Ventures, illustrates this. Before COVID-19, in March 2020, earnings of most platform workers were comparable to those of middle-to-high income, urban households. But with COVID-19 and lockdowns disrupting livelihoods everywhere, we see a drastic fall in most of their incomes by August 2020, descending to levels comparable to those of low-income, urban households (Table 1).

This income volatility, sometimes caused by external factors like macroeconomic shocks and at other times by internal factors like changing of payment and incentive structures by platforms, is one of the many reasons why platform workers face challenges very similar to those of other urban, low-income households, even though they are not always technically low-income.

Some recent surveys have tried to study the finances of platform workers exclusively. India Spotlight Survey, mentioned before in this post, assesses the impact of COVID-19 on the living and working conditions of platform workers while also taking stock of their financial goals and vulnerabilities. Another joint survey by Economic Times and Bon Credit tries to explore their demographic and financial profiles and assess their financial well-being. These surveys highlight the many financial challenges that platform workers face and the negative coping mechanisms they often must rely on to tide over distress.

But there is still a lot more that remains to be explored about the finances of platform workers and their households:

- How volatile are their incomes and how frequent is this volatility?

- How do they manage their finances during periods of surplus and distress

- Whether they see platform work as their main source of livelihood or as an additional gig they do for extra earnings?

- Whether platform work itself is their aspirational work or just a stepping stone towards other aspirational work?

- What are their medium-to-long term financial goals and what kinds of vulnerabilities are inhibiting them from achieving these goals?

- What kind of financial instruments and safety nets exist, and what suitable additions to these can help them reach their goals by overcoming their vulnerabilities?

- Whether and how answers to the above questions vary with male and female platform workers, with those working in different segments of the platform economy, and with those in different stages of their household lifecycle?

- What are the implications of the broader labour market structures on their work and finances?

Answering these questions is crucial to enrich our knowledge about platform workers and their financial livelihoods, and to design suitable interventions, in the form of customised financial instruments and social protection measures, that can improve their overall financial well-being. While longitudinal surveys can by design only scratch the surface, getting meaningful answers to these questions requires more rigorous studies on the day-to-day finances of different kinds of platform workers.

Further reading: Literature Review on the Finances of Gig Workers on the Dvara Research Blog.

References

[1] The Digital Hustle: Flourish Ventures India Spotlight (full report)

[2] Report of the Household Finance Committee, Reserve Bank of India (full report)

[3] Op-Ed: What India’s informal sector needs right now, The Indian Express (read article)

[4] State of Working India 2021 (full report)

Rakshith is a Research Associate with the Household Finance Research Initiative. He has completed his Master’s degree in Public Policy from National Law School of India University, Bengaluru.

In-Depth is a blog series by OMI on the latest mobility-related developments.